Massachusetts’ ban of flavored tobacco products is not the success its proponents make it out to be, according to Ulrik Boesen of the Tax Foundation.

While a study published in JAMA Internal Medicine found that the sale of flavored tobacco in Massachusetts decreased more than in 27 control states in the wake of the state ban, the authors failed to consider the impact of cross-border trade.

According to Boesen, increased sales in neighboring New Hampshire and Rhode Island almost completely made up for the decrease in Massachusetts.

“The end result of the ban, in fact, is that Massachusetts is stuck with the societal costs associated with consumption, while the revenue from taxing flavored tobacco products is being raised in neighboring states,” Boesen wrote on the Tax Foundation’s website.

Looking at the New England region as a whole confirms that the flavor ban did not work as intended, according to Boesen. “Sales moved around rather than disappeared, and the ban evidently did not impact consumption,” he wrote. “Total sales for the region decreased by slightly more than 1 percent comparing the 12 months preceding the ban to the 12 months following the ban—largely comparable to the national sales trends.”

Last year, a study by the New England Convenience Store and Energy Marketers Association (NECSEMA), found excise tax lost income in Massachusetts from selling fewer menthol cigarettes alone amounted to $62 million in the first six months of the ban. No specific figures were given for electronic nicotine delivery systems in the release for that study.

The previous study also found that losses simply transferred to Massachusetts’ neighboring states. Cigarettes excise tax stamp sales dropped 23.9 percent in Massachusetts while New Hampshire gained $28,574,340 or 29.7 percent. Rhode Island gained $12,100,000 or 18.2 percent in excise taxes.

The previous study’s estimated Massachusetts loss including the sales tax is $73,008,000 while Rhode Island saw a gain of $14,066,740.

As the U.S. Food and Drug Administration and other states consider Massachusetts’ example, Boesen urges lawmakers to think twice before banning flavored tobacco products. “The experience out of Massachusetts has not been a success story and other states should be wary of conducting their own expensive experiments,” he wrote.

Experts say Congress’ latest attempt to tax nicotine is complicated, confusing and harmful to public health.

By Timothy S. Donahue

To help pay for an infrastructure bill, the U.S. Congress has again introduced an excise tax on next-generation nicotine products, such as e-cigarettes and snus. The excise tax would apply to nicotine vapor products using both natural and synthetic nicotine as well as nicotine pouches. Experts say the provision, which would ultimately be paid by tobacco consumers, goes against U.S. President Biden’s campaign promise to not increase taxes on those making less than $400,000, negatively impact tobacco harm reduction efforts, increase sales of combustible tobacco products and boost an already growing black market.

The nicotine tax has been removed and reintroduced to Biden’s Build Back Better (BBB) legislation at least three times. The proposed vapor tax provision is now part of the latest version of the administration’s social spending and climate bill. According to Ulrik Boesen, a senior policy analyst with the Center for State Tax Policy at the Tax Foundation, taxes on tobacco and nicotine products tend to serve at least two purposes: to improve public health and raise revenue. He claims that a nicotine tax could do that if it is properly designed.

Ulrik Boesen / Credit: Tax Foundation

“A good design means internalizing externalities related to consumption of a product,” Boesen stated. “With tobacco and nicotine product consumption, these externalities are the health risks connected to frequent use and [the] quantity consumed. Nicotine is the addictive substance in the products but not the harmful ingredient. In other words, the proposal does not target the harmful behavior directly.”

Taxing based on nicotine content would favor low-nicotine liquids and could encourage increased consumption in the quantity of liquid, according to Boesen. “For example, a vapor pod that has a nicotine content of 3 percent and contains 1 mL of liquid would be taxed at $0.83 whereas a vapor pod that has a nicotine content of 5 percent and also contains 1 mL of liquid would be taxed at $1.39 even if there is no difference, or even a negative differential, in broader health effects of the two pods,” he states, adding that the effects of the tax are most substantial for nicotine pouches, such that the category is unlikely to survive.

Other estimates show that a 60 mL bottle of e-liquid with 12 mg of nicotine e-liquid would be taxed at $20.02. A four-pack of 8 mL pods with 5 percent nicotine salt pods would be taxed at $4.45 and a 15-pouch can of 8 mg nicotine pouches would be taxed at $3.34 (alongside state and local taxes, the cost of a single can could grow to $20 in some states).

Bryan Haynes, a partner with the law firm Troutman Pepper who specializes in tobacco and vapor regulations, said that, at a minimum, the proposed nicotine tax is “a hastily written addition” that will “have a negative impact on tobacco harm reduction efforts and public health.” He said that it’s the first time the tobacco industry has seen an excise tax placed on an ingredient instead of a finished good. “This is an unprecedented type of tax that will ultimately drive former smokers back to combustible products,” said Haynes, adding that taxing an ingredient could also cause unforeseen issues for manufacturers, such as moving material between factories.

Bryan Haynes / Credit: Troutman Pepper

“If a company is producing nicotine or even synthetic nicotine, moving product from one factory to another could trigger the need for an Alcohol and Tobacco Tax and Trade Bureau (TTB) license, and when product is removed, so to speak, from their factory, they would be responsible for remitting the taxes,” explained Haynes. “There may be a way, for example, if the company removed the nicotine from their factory and transported it in-bond to another TTB factory that you could make that work. But it’s just not clear. There is the potential for a lot of unforeseen issues to arise the way the tax is currently being proposed.”

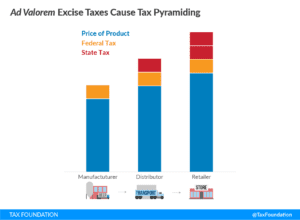

States often tax nicotine products by its cost. Boesen says the tax on the product will pyramid since the federal tax would be levied at the manufacturer level and the state tax is levied at the distribution level. “In effect, the state tax base includes the federal tax and becomes a tax on a tax. This means that even if the taxes on tobacco and other nicotine products are approximately equal at the federal level, by the time it reaches the consumer, the nicotine product will carry a higher tax (and often a higher price),” he states. “This is highly problematic when considering that cigarettes are much more harmful than nicotine products. That makes the federal tax proposal look like a harm-maximizing strategy.”

Credit: Tax Foundation

The bill also subjects synthetic nicotine products to the nicotine tax. Many in the industry have expressed concern that this provision could allow the U.S. Food and Drug Administration to assert authority over the substance. Synthetic nicotine is covered not only in the proposed tax bill but also in the Prevent All Cigarette Trafficking (PACT) Act, which bans the U.S. Postal Service from mailing any vaping products.

Azim Chowdhury, a partner at the law firm Keller and Heckman who specializes in vapor, nicotine and tobacco product regulation, said that’s just not possible and Haynes agrees. “The definition of a tobacco product in the Tobacco Control Act (TCA) is clear. It’s just not ambiguous; a product must be made or derived from tobacco, or a component or part of a tobacco product, to be a tobacco product,” said Chowdhury.

Azim Chowdhury

“Congress would have to change the Tobacco Control Act’s definition of a tobacco product in order to give FDA’s Center for Tobacco Products the authority to regulate synthetic nicotine products as tobacco products. That won’t happen overnight. I also see a scenario where synthetic nicotine could be regulated as a drug and that would be a whole different and more onerous regulatory regime.”

The FDA could, however, cite the inclusion of synthetic products in the PACT Act and the latest nicotine tax proposal in its lobbying efforts to change the TCA’s definition of tobacco, said Haynes. “I could see the FDA telling Congress, ‘You just amended the Internal Revenue Code to make these products subject to federal excise taxes just like tobacco-derived nicotine, so it’s not a big stretch to amend the Tobacco Control Act’ in the same way,” he explains. “That’s how I would do it. It’s not really a legal argument, but it could be a decent lobbying argument.”

It isn’t just vapers, business owners and attorneys that find fault with the proposed nicotine tax; researchers suggest the tax could also harm public health. Michael Pesko, an associate professor in the Department of Economics at Georgia State University, used a $1.4 million dollar grant from the National Institutes of Health (NIH) to conduct e-cigarette policy evaluation research, including the evaluation of e-cigarette taxes (Pesko receives no funding from the tobacco industry or related groups). Pesko found that e-cigarettes and other nicotine vaping products function as what economists call “substitutes” for conventional cigarettes.

“In practical terms, if e-cigarettes and cigarettes are substitutes, then raising the price of one on average leads people to increase use of the other. Given extensive peer-reviewed evidence indicating that these products are substitutes, an unintended but inevitable effect of increasing taxes on e-cigarettes is to increase cigarette use,” Pesko said. “Given that cigarettes are believed to be substantially more harmful than e-cigarettes, this effect on [combustible] cigarette use is concerning …. A wide array of research suggests that this boost in cigarette use as a result of large e-cigarette tax increases would significantly increase overall tobacco-related death and disease.”

Michael Pesko / Credit: GSU

These findings prompted Pesko to send a letter to Congress concerning the proposed vape tax. In the letter, he states that his research team’s economic evaluations of existing state and county e-cigarettes taxes found that increasing e-cigarette taxes to parity with the combustible cigarette tax rate would “sizably increase cigarette use across teens, adults and pregnant women compared to taxing tobacco products differentially in proportion to their health risk.”

Pesko said researchers found several concerning consequences of large e-cigarette tax increases:

Simulating the current bill’s e-cigarette tax on teen tobacco use indicates that this policy would reduce teen e-cigarette use by 2.7 percentage points but that two in three teens who do not use e-cigarettes due to the tax would smoke cigarettes instead. This would result in approximately a half million extra teenage smokers overall. This finding that teens substitute to cigarettes in response to e-cigarette taxes has also been documented using National Youth Tobacco Survey data.

The tax would raise the number of daily adult cigarette smokers by 2.5 million nationally and reduce adult e-cigarette users by a similar number.

For every e-cigarette pod eliminated by an e-cigarette tax, more than 5.5 extra packs of cigarettes are sold instead.

For every three pregnant women that do not use e-cigarettes due to an e-cigarette tax, one smokes cigarettes instead (study).

Pesko told Vapor Voice he was surprised to find that increased e-cigarette tax consistently resulted in substitution across various data sources. “And the magnitudes are fairly sizable,” he noted. “This is an unusual level of accordance for academic research.” Pesko believes that any tax on nicotine products should be based on quantity.

Boesen agreed. He stated that for vapor products, the “obvious choice” is taxing the liquid by volume (per mL), and for nicotine pouches, a tax by weight or per pouch is a straightforward solution. “It is the administratively simplest and most straightforward way for the federal government to tax these goods as it does not require valuation and as such does not require expensive administration,” he stated. “The nicotine tax proposal in the Build Back Better Act neglects sound excise tax policy design and by doing so risks harming public health. Lawmakers should reconsider this approach to nicotine taxation.”

Chowdhury said that the industry must do more and that interested stakeholders and consumers should reach out and push back on the nicotine tax because it will be devastating to the vapor industry. “It seems like the general industry feels like [this nicotine tax] won’t get through somehow, that some people will prevent it from being in the final bill, but I think it’s a huge risk,” said Chowdhury. “Without serious pushback, it could end up there; it could very well end up becoming law.”

Haynes said that if the nicotine tax bill ever makes it to Biden’s desk, “he’s going to sign it.”

A proposed tax bill in U.S. Congress would add $40 to the cost of a 120 mL bottle of e-liquid with 6 mg of nicotine.

By VV staff

The proposed U.S. Tobacco Tax Equity (TTE) Act would tax vaping products the same as combustible cigarettes. According to research from the Tax Foundation, an independent tax policy nonprofit, the proposal would double the rates on combustible cigarettes and increase the rates on all other tobacco and nicotine products—including electronic nicotine-delivery systems (ENDS)—to achieve parity with the traditional tobacco tax rate.

The proposed rule aims for the tax per 1,000 cigarettes to be increased to $100.66. Vaping products would be taxed at this same rate, with 1,000 cigarettes being equal to 1,810 mg of nicotine.

“In addition to the one-time increase, the rates would be indexed to inflation, which means they would automatically increase every year,” the report states. “According to Tax Foundation estimates, the tax increases would raise $112 billion over 10 years. The bulk of the revenue, $74.8 billion, is from the doubling of cigarette taxes. The tax on vapor products would raise roughly $15 billion over 10 years.”

According to Alex Norcia of Filter, the proposal would benefit large corporations and traditional tobacco products while unfairly hurting people in lower socioeconomic classes as most smokers do not typically belong to the upper classes. Current cigarette smoking in the United States “is higher among people with low annual household income than those with higher annual household incomes,” according to the U.S. Centers for Disease Control and Prevention.

“This means that a 30 mL bottle of e-liquid containing 3 mg of nicotine per milliliter would be subject a tax rate of $5 for the bottle. A 120 mL bottle of e-liquid that contains 6 mg of nicotine per milliliter would attract a tax rate of $40 for the bottle,” writes Norcia. “In comparison, critics and tax reformists have estimated that a four-pack of Juul pods would be taxed around $9—giving a clear advantage to a giant over the smaller player. More alarmingly, a pack of cigarettes would only be taxed around $2, creating an incentive for nicotine users to pick cigarettes over less risky vapor products.”

In an interview with C-Span on Sept. 15, White House Press Secretary Jen Psaki was asked if the White House believes that the proposed bill on taxing tobacco/vaping products would violate President Biden’s promise to not raise taxes on those making under $400,000 per year. She replied, “No, we don’t,” adding that it was “just one of the ideas out there.”

Vape shops are saying that the proposed tax increase would “completely destroy” their businesses, saying it would be even worse than the U.S. Food and Drug Administration’s failure to approve any ENDS products by the Sept. 9 deadline (see “Authorization Denied,” page?) and the issuing of hundreds of marketing denial orders (MDOs).

“This is going to more than double, and in some cases triple or quadruple, the price of liquids that I sell,” Keith Gossett, the owner of Bucky’s Vape Shop in Columbus, Georgia, told Reason. “I’m going to sit there and try to tell a man with a $6 pack of cigarettes that my [$75] product is better. This tax will close my shop.”

Rather than protecting public health, high excise taxes on lower risk tobacco products jeopardize public health by pushing consumers back to smoking combustible products, according to the Tax Foundation report. “If the policy goal of high taxes on cigarettes is to encourage cessation, taxation of other tobacco and nicotine products must be considered a part of that policy design,” the report states.

The last time the federal excise tax on tobacco was increased was in 2009. While the federal tax has not changed for 12 years, the average tax paid by consumers has increased drastically. Including the last federal increase, the average combined state and federal excise tax rate on tobacco products has jumped more than 80 percent (the average state excise tax rate increased 65 percent between 2009 and 2021), according to the Tax Foundation.

The proposed U.S. Tobacco Tax Equity (TTE) Act would tax vaping products the same as combustible cigarettes. According to research from the Tax Foundation, an independent tax policy nonprofit, the proposal would double the rates on combustible cigarettes and increase the rates on all other tobacco and nicotine products – including electronic nicotine-delivery systems (ENDS) – to achieve parity with the traditional tobacco tax rate.

Credit: TS Donahue

The proposed rule aims for the tax per 1,000 cigarettes to be increased to $100.66. Vaping products would be taxed at this same rate, with 1,000 cigarettes being equal to 1,810 milligrams of nicotine.

“In addition to the one-time increase, the rates would be indexed to inflation, which means they would automatically increase every year,” the report states. “According to Tax Foundation estimates, the tax increases would raise $112 billion over 10 years. The bulk of the revenue, $74.8 billion, is from the doubling of cigarette taxes. The tax on vapor products would raise roughly $15 billion over 10 years.”

According to Alex Norcia of Filter, the proposal would benefit large corporations and traditional tobacco products, while unfairly hurting people in lower socioeconomic classes as most smokers do not typically belong to the upper classes. Current cigarette smoking in the United States “is higher among people with low annual household income than those with higher annual household incomes,” according to the Centers for Disease Control and Prevention.

“This means that a 30-milliliter bottle of e-liquid containing 3 milligrams of nicotine per milliliter would be subject a tax rate of $5 for the bottle. A 120-milliliter bottle of e-liquid that contains 6 milligrams of nicotine per milliliter would attract a tax rate of $40 for the bottle,” writes Norcia. “In comparison, critics and tax reformists have estimated that a four-pack of Juul pods would be taxed around $9—giving a clear advantage to a giant over the smaller player. More alarmingly, a pack of cigarettes would only be taxed around $2, creating an incentive for nicotine users to pick cigarettes over less-risky vapor products.”

Credit: Tax Foundation

The TTE Act as part a massive $3.5 trillion spending bill appear to be heading for a collision with President Joe Biden’s pledge not to raise taxes on America’s middle class. In an interview with C-Span on Sept. 15, White House Press Secretary Jen Psaki was asked if the White House believes that the proposed bill on taxing tobacco/vaping products would violate Biden’s promise to not raise taxes on those making under $400,000 per year. She replied, “No, we don’t,” adding that it was “just one of the ideas out there.”

Vape Shop owners are saying that the proposed tax increase would “completely destroy” their businesses, saying it would be even worse than the U.S. Food and Drug Administration’s failure to approve any ENDS products by the Sept. 9 deadline and the issuing of nearly 200 marketing denial orders (MDOs).

“This is going to more than double, and in some cases triple or quadruple, the price of liquids that I sell,” says Keith Gossett, the owner of Bucky’s Vape Shop in Columbus, Georgia, told Reason. “I’m going to sit there and try to tell a man with a $6 pack of cigarettes that my [$75] product is better. This tax will close my shop.”

The last time the federal excise tax on tobacco was increased was in 2009. While the federal tax has not changed for 12 years, the average tax paid by consumers has increased drastically. Including the last federal increase, the average combined state and federal excise tax rate on tobacco products has jumped more than 80 percent (the average state excise tax rate increased 65 percent between 2009 and 2021), according to Tax Foundation.